In just a few short years, artificial intelligence (AI) has become a cornerstone of modern finance, fundamentally reshaping how institutions, businesses, and individuals interact with money. At the forefront of this revolution are AI-powered apps that leverage advanced algorithms, machine learning, and real-time data analysis to provide faster, more efficient, and more personalized financial solutions than ever before. By breaking down barriers and optimizing decision-making processes, these applications are paving the way for a new era of financial management, from personal banking to corporate investments.

1. A New Era of Personalized Banking

One of the most immediate ways AI apps have changed finance is through personalized banking experiences. Traditionally, consumers would rely on branch visits, phone calls, or static online portals to manage their accounts. AI-driven apps, on the other hand, take financial management to a whole new level by tailoring advice, alerts, and suggestions to individual needs and habits. For example, many popular banking apps now integrate AI chatbots that can answer questions in real-time, predict upcoming expenses, or recommend budget adjustments based on your transaction history.

This level of personalization goes far beyond simple notifications. AI apps analyze spending patterns and savings goals to create custom financial plans. They provide early warnings about cash flow issues, suggest cost-cutting measures, and even highlight investment opportunities that align with the user’s risk tolerance and long-term objectives. By turning vast amounts of transactional data into actionable insights, these apps enable users to make smarter financial decisions without needing advanced financial literacy.

2. Revolutionizing Lending and Credit Scoring

AI apps have also dramatically improved the way lending and credit scoring are conducted. In the past, obtaining a loan or credit card often involved lengthy paperwork, manual credit checks, and days—if not weeks—of waiting for approval. Today, AI-powered applications streamline this process by analyzing thousands of data points in seconds. Instead of relying solely on traditional credit scores, these systems incorporate alternative data sources such as utility payments, rent history, and even social media behavior to produce more accurate credit assessments.

This shift benefits both lenders and borrowers. For lenders, AI models can identify risk factors more precisely, reducing default rates and enabling them to offer competitive rates. For borrowers, it opens up financial opportunities to people who may have been overlooked by conventional credit models. Gig economy workers, freelancers, and individuals with limited credit histories can now access loans more easily because AI takes a more holistic view of their financial stability. In essence, these AI-driven lending platforms expand financial inclusion and create a more equitable lending environment.

3. Investment and Wealth Management at Your Fingertips

The world of investing has traditionally been dominated by seasoned professionals and complex financial institutions. But AI-powered investment apps have democratized access to the markets, empowering individuals to manage their portfolios with confidence. Robo-advisors, for instance, use advanced algorithms to provide automated, data-driven investment strategies. These apps assess a user’s risk tolerance, financial goals, and market conditions to recommend a diversified portfolio of stocks, bonds, and other assets—all without the need for a human financial advisor.

In addition to robo-advisors, AI investment apps are also leveraging natural language processing (NLP) and sentiment analysis to gauge market sentiment in real-time. They scour social media platforms, news outlets, and financial reports to identify trends and anticipate market movements. By delivering these insights directly to users’ smartphones, AI apps ensure that everyday investors can stay informed and make timely decisions.

Moreover, these platforms offer continuous optimization. AI systems learn from market behavior and adjust strategies dynamically, ensuring that portfolios remain aligned with long-term objectives even as conditions change. The result is a more accessible, cost-effective, and efficient approach to wealth management that was previously unavailable to the average investor.

4. Enhancing Fraud Detection and Cybersecurity

As finance becomes increasingly digitized, the risk of fraud and cyberattacks has grown. Fortunately, AI apps have stepped in to provide a robust line of defense. Machine learning models excel at detecting unusual patterns and behaviors that may indicate fraudulent activity. By analyzing billions of transactions, these systems can identify anomalies—such as sudden large withdrawals, unexpected location changes, or unusual login times—and flag them in real-time.

Banks and payment providers have integrated these AI systems into their apps to protect consumers and businesses alike. If an app detects a suspicious transaction, it can instantly notify the user, lock the account, and prompt further verification. This proactive approach minimizes losses, improves trust, and ensures that financial platforms remain secure.

Additionally, AI-powered fraud prevention tools continuously evolve. The more data they process, the better they become at distinguishing between legitimate and malicious activities. Over time, these systems adapt to new tactics used by fraudsters, maintaining a secure environment even as threats evolve. This level of adaptability has become a critical asset for both consumers and financial institutions in the digital age.

5. Streamlining Regulatory Compliance and Risk Management

For financial institutions, staying compliant with a complex web of regulations is a constant challenge. AI applications have eased this burden by automating compliance processes, reducing human error, and ensuring that institutions stay in line with legal requirements. By analyzing data and generating reports in real-time, these apps help banks quickly identify potential compliance issues and address them before they escalate.

Risk management has also been transformed by AI. In the past, risk assessments often relied on periodic reviews and historical data. AI-driven risk management tools, however, provide continuous monitoring and real-time risk modeling. By evaluating market conditions, geopolitical events, and internal financial data, these systems can predict potential risks and recommend proactive measures to mitigate them. This enables financial institutions to respond more quickly to emerging threats and maintain stability, even during times of uncertainty.

6. Empowering Small Businesses and Entrepreneurs

Small businesses have traditionally faced significant barriers when it comes to accessing financial services and tools. AI-powered finance apps have broken down many of these barriers by offering affordable, user-friendly solutions. For instance, expense-tracking apps can automatically categorize transactions, generate detailed financial reports, and provide real-time cash flow insights. These features enable small business owners to manage their finances more effectively, make informed decisions, and plan for growth.

Beyond day-to-day financial management, AI apps also assist small businesses with securing funding. By analyzing the company’s cash flow, customer base, and market conditions, these applications can match businesses with suitable loan options or investor opportunities. This targeted approach not only saves time but also increases the likelihood of securing the necessary capital.

7. The Future of AI-Driven Financial Innovation

As AI technology continues to advance, its impact on the financial world will only grow. In the future, we can expect even more sophisticated AI-powered apps that integrate seamlessly into our daily lives. Voice-activated financial assistants, augmented reality tools for financial planning, and fully automated financial ecosystems are all on the horizon.

At the same time, the widespread adoption of AI in finance raises important questions about ethics, transparency, and data privacy. As these apps become more influential, ensuring that they operate fairly and responsibly will be essential. Regulators, developers, and users must work together to strike a balance between innovation and accountability.

Conclusion

AI-driven apps have ushered in a new era of financial transformation. By providing personalized banking experiences, streamlining lending processes, democratizing investing, enhancing fraud detection, and empowering small businesses, these applications have made finance more accessible, efficient, and secure. As the technology evolves, it will continue to redefine how we manage, grow, and protect our money, ultimately reshaping the financial landscape for years to come.

It all started on a regular day, nothing out of the ordinary. I woke up, made my coffee, and scrolled through my phone like everyone else. But what happened next changed my perspective on everything.

I wasn’t expecting much when I stumbled upon something that, at first, seemed completely ordinary. You know that feeling when you see something and think, “Oh, that’s interesting,” but then you move on? That’s exactly what I did. But for some reason, I kept thinking about it.

Curiosity got the best of me. I decided to dig deeper. What I found left me completely speechless. I tried to tell my friends, my family, even strangers online—but nobody believed me.

At first, I thought maybe I was overreacting. Maybe I had misunderstood. But as I went further down the rabbit hole, the pieces started to come together in a way that made too much sense. It wasn’t just some coincidence. It was real, and I was right in the middle of it.

The First Signs

The first thing that made me pause was how perfectly everything lined up. I had read about strange occurrences before, but this was happening to me in real time. I started noticing small, almost imperceptible details that, when put together, painted a much bigger picture.

I tried to tell a close friend about it. Their reaction? Laughter. They thought I was joking or exaggerating. “That can’t be real,” they said. “You’re overthinking it.”

But I wasn’t.

I decided to test it out for myself. I followed every little step that led me to that moment, trying to see if it was just a fluke. It wasn’t.

The Deeper I Went, The Stranger It Got

It became an obsession. I needed answers. Every time I thought I had figured it out, another layer appeared. The more I tried to explain it to others, the more they dismissed me.

I started keeping track of everything. Notes, screenshots, even voice recordings. I had proof, undeniable proof, but somehow, even when I presented it, people shrugged it off. “That’s impossible,” they said.

But it wasn’t impossible. It was happening.

The Turning Point

One night, I decided to take things further. I wanted to go beyond just observing—I wanted to see what would happen if I really leaned into it. That’s when things got really strange.

What I found out is something I can’t just explain in a single sentence. It’s something that has to be experienced to be fully understood. Once you see it, you can’t unsee it.

It’s not magic, and it’s not some conspiracy. It’s real, and it’s happening whether people want to believe it or not.

Why Nobody Believes Me

Maybe it’s because it sounds too good to be true. Maybe it’s because people don’t want to accept that something so unexpected could actually work. Maybe it’s just easier to stay in the comfort of what’s familiar.

But the truth is, just because something sounds unbelievable doesn’t mean it’s not real.

I’ve given up trying to convince people. Instead, I just tell them: see for yourself.

And when they finally do, their reaction is always the same.

Banks have long been pillars of the financial world, trusted institutions where most of us deposit our hard-earned money, apply for loans, and rely on convenient services. They offer a veneer of reliability, complete with reassuring advertisements, user-friendly apps, and a polished customer service approach. But behind the glossy exterior lies a world that most consumers never see—one filled with hidden fees, questionable practices, and a reliance on public ignorance to maintain profitability. These are the secrets banks would prefer you never find out.

1. The True Cost of “Free” Accounts

One of the most appealing hooks banks use to attract customers is the promise of “free” checking or savings accounts. However, these so-called “free” accounts often come with strings attached—such as minimum balance requirements, direct deposit mandates, or limits on the number of transactions. Should you fail to meet these requirements, you’ll be hit with monthly maintenance fees, penalty charges, or transaction fees. What’s more, the terms can change with minimal notice, meaning an account you thought was cost-free can suddenly start draining money from your balance.

Over time, these charges add up. Even small monthly fees can amount to hundreds of dollars annually, eroding your savings and making it harder to build financial stability. Banks rely on the fact that many customers won’t closely monitor their statements or fully understand the terms of their accounts. This lack of transparency allows them to quietly profit from fees that seem inconsequential on their own, but collectively become a significant revenue stream.

2. The Overdraft Fee Trap

Another common source of frustration and financial drain is overdraft fees. While banks often present overdraft protection as a helpful safety net—ensuring that important transactions are not declined—this service comes at a steep cost. Many consumers don’t realize that even a small overdraft can trigger a large fee, often upwards of $35 per transaction. Worse, some banks intentionally reorder transactions to maximize these fees.

For example, rather than processing smaller transactions first, a bank might process the largest payment first, causing your account to go negative sooner. Then, each subsequent smaller transaction generates an additional overdraft fee. This practice turns what might have been a single fee into multiple charges, leaving customers scrambling to cover the losses.

3. The Low Interest Rate Illusion

Savings accounts are marketed as a safe way to grow your money. But while banks may use your deposits to issue loans at rates of 5% or higher, the interest they offer you in return often amounts to a fraction of a percent. This discrepancy means that your money is effectively losing value over time, especially when inflation is factored in.

Why don’t banks share more of the profits from your deposits? Quite simply, because they don’t have to. With most customers unaware of alternative options—such as high-yield savings accounts from online banks or credit unions—traditional banks face little pressure to increase their rates. As a result, they pocket the majority of the earnings while you see only minimal growth in your account balance.

4. The Murky World of Fees and Penalties

Beyond maintenance and overdraft fees, banks have a laundry list of other charges that can quietly eat into your funds. Foreign transaction fees, wire transfer fees, ATM fees for using out-of-network machines, early withdrawal penalties on certain accounts—the list goes on. What makes these fees so insidious is how easily they go unnoticed.

For instance, you might withdraw cash from an ATM, unaware that both the ATM’s operator and your bank will charge separate fees. Or you might transfer money internationally only to find that a small percentage of your funds never reached the recipient because of hidden conversion costs. These small, scattered charges are rarely explained up front and often buried in fine print. Only those who scrutinize every line of their monthly statement will catch them, and even then, most people feel powerless to contest such charges.

5. Data Monetization: Your Information as a Product

When you think of a bank’s “products,” you might imagine loans, mortgages, and credit cards. But there’s another product they quietly profit from: your data. Banks have access to a treasure trove of personal information—your spending habits, income level, investment choices, and more. While they may not sell your information outright, banks often use aggregated, anonymized data for analysis or share it with third-party partners.

This data is highly valuable. It helps banks refine their own marketing strategies, tailor product offerings, and even predict economic trends. But for the consumer, it raises privacy concerns. If your spending habits are being analyzed and shared—sometimes without explicit consent—what does that mean for your control over your personal information? Most customers have no idea that their data is being used in these ways, and banks have little incentive to be upfront about it.

6. The Complex Web of Credit Cards

Credit cards are both a blessing and a curse. They offer convenience, rewards points, and the ability to build credit history. But they also come with high interest rates, late payment fees, and terms that are intentionally difficult to understand. Banks rely on the fact that many consumers don’t fully grasp how credit card interest is calculated. As a result, people end up paying far more in interest and fees than they expect.

Another tactic is the enticing “introductory rate” that skyrockets after a few months. Customers are drawn in by offers of 0% APR for the first six months, only to see their rates jump to 20% or higher once the promotional period ends. Coupled with late fees and penalty APRs, these cards become a significant source of revenue for banks.

7. The Predatory Loan Cycle

Banks know that loans are a critical tool for most consumers. Whether it’s a mortgage, auto loan, or personal loan, these products can help people achieve their goals. But many loans come with terms that are designed to keep borrowers locked in for as long as possible. Prepayment penalties, adjustable rates that increase over time, and lengthy repayment schedules all ensure that customers continue paying interest for years—often longer than necessary.

For example, a borrower might refinance their mortgage to get a lower monthly payment, only to discover that the new loan includes hidden fees or resets the clock on the term, meaning they’ll pay interest for even more years. Banks don’t emphasize these long-term costs; they focus on the short-term savings that appeal to borrowers in the moment.

8. Resistance to Regulatory Oversight

You might wonder why banks can get away with so many of these practices. A key reason is their powerful lobbying efforts and resistance to stricter regulations. The financial industry spends billions annually on lobbying to influence lawmakers and regulators. They argue that heavy-handed rules would stifle innovation or reduce customer choice, but in reality, many of these regulations are designed to protect consumers from the very practices outlined here.

By opposing transparency requirements, fighting against fee caps, and lobbying for looser data-sharing rules, banks maintain the status quo. Meanwhile, the average consumer continues to face hidden costs, confusing terms, and opaque practices.

9. The Bailout Bonus Problem

When the global economy falters and banks run into trouble, governments often step in to provide bailouts. These bailouts are intended to stabilize the financial system and protect ordinary consumers’ deposits. But in some cases, bailout funds have been used to pay massive bonuses to top executives—executives whose decisions may have contributed to the financial instability in the first place.

This misuse of taxpayer money not only erodes public trust but also reinforces the idea that banks operate with one set of rules for themselves and another for everyone else. While ordinary customers struggle to recover from economic downturns, high-level bankers often emerge unscathed, financially secure thanks to generous bonuses.

10. The Illusion of Security

Banks present themselves as the safest places to store your money. And while your deposits are generally protected by insurance (such as FDIC coverage in the U.S.), other areas of banking are less secure than you might think. Fraud protection policies vary, and in some cases, customers may find it difficult to recover stolen funds. Additionally, the push toward digital banking introduces new vulnerabilities.

Cyberattacks, data breaches, and phishing scams are constant threats, and while banks invest heavily in security measures, they rarely emphasize the risks to consumers. Instead, they project an image of unshakeable safety, leaving customers with a false sense of security.

Conclusion

The more you understand about how banks operate behind the scenes, the better equipped you’ll be to protect yourself. By knowing the hidden fees, scrutinizing terms and conditions, exploring alternative financial products, and advocating for greater transparency, you can avoid falling victim to the secrets banks don’t want you to know. While these institutions are vital to the economy, they’re also profit-driven entities that benefit from a lack of consumer knowledge. The first step to leveling the playing field is to uncover these truths and make informed financial decisions.

Banks have long stood at the heart of the global economy, serving as intermediaries for loans, savings, and investments. For many, they represent stability, reliability, and security. But while banks tout their customer-focused slogans and convenient digital tools, the reality behind their operations often tells a more complex story—one that banks would prefer the average consumer not fully understand. These institutions don’t just earn money by holding deposits or making straightforward loans; they thrive on practices that generate additional revenue streams, often at the expense of everyday consumers.

In this detailed exploration, we’ll uncover the top ten “dirty secrets” banks would rather keep under wraps. From hidden fees to data selling, these are the practices that not only frustrate consumers but can also erode trust in the financial system. By shining a light on these issues, we aim to empower you with the knowledge needed to navigate the banking landscape more wisely.

1. Exorbitant Hidden Fees

For many consumers, checking and savings accounts appear straightforward on the surface—deposit money, make withdrawals, pay the occasional ATM fee. But dig deeper into the fine print, and you’ll find a litany of hidden charges that can quickly add up. Monthly maintenance fees, paper statement fees, overdraft protection fees, and foreign transaction fees are just the start. These charges often hit customers without warning, eroding savings over time and disproportionately impacting those who are already struggling financially.

Consider the average checking account. Many banks promote “free” accounts but require minimum balances to avoid fees. If a customer falls below that threshold, they’re hit with monthly maintenance fees that can range from a few dollars to over $15. In practice, these fees mean that those who can least afford them—students, low-income workers, or retirees—end up paying for services they were told would be free. Some banks also bundle their fees into complicated statements, making it difficult for account holders to pinpoint where their money is going. This lack of transparency allows banks to collect billions annually from fees alone.

2. Misleading Loan Terms

Loans are essential financial products, enabling everything from home purchases to college education. But behind the friendly offers of low rates and flexible terms lies a maze of fine print that can trap borrowers. Banks often advertise their loans with the lowest possible rates—rates that only a small percentage of borrowers with near-perfect credit scores can qualify for. Everyone else ends up paying higher interest rates, often without realizing it until it’s too late.

For instance, many credit cards and personal loans come with teaser rates: a promotional low interest rate that jumps sharply after an introductory period. Borrowers who don’t fully understand the terms may find themselves paying twice or three times as much in interest once the promotional period ends. Additionally, banks often include prepayment penalties, meaning that if a borrower tries to pay off their loan early, they’re hit with additional fees. This ensures that banks continue to collect interest revenue, even when customers act responsibly.

3. Manipulative Overdraft Practices

Overdraft fees are another major revenue source for banks, and they’ve devised clever ways to maximize them. While overdraft protection is often marketed as a helpful service, in reality, it frequently results in a cascade of fees for customers who might have preferred a declined transaction instead. Even worse, some banks reorder transactions—processing the largest transactions first rather than in the order they occurred. This strategy depletes account balances faster, triggering multiple overdrafts and, consequently, multiple fees.

For example, if you have $50 in your account and make four transactions of $5 followed by one $45 transaction, banks may process the $45 first. This leaves the account overdrawn for the smaller transactions, resulting in four separate overdraft fees instead of just one. While some banks have begun to curb these practices under public and regulatory pressure, many still rely on overdraft fees as a major profit center.

4. Selling Customer Data

Your banking habits reveal a lot about you: where you shop, how often you travel, what subscriptions you maintain, and more. Banks have access to this valuable data, and they’re not always discreet about how they use it. While they might not sell your personal details outright, many engage in data-sharing agreements or partnerships with third-party advertisers and data brokers. This means your transaction history can be analyzed, packaged, and used to target you with marketing or promotions.

Even if banks claim to anonymize data, patterns can still be tied back to individual consumers. For example, a record showing frequent transactions at a particular grocery store or gym can enable advertisers to target you based on your spending habits. While many banks offer opt-out options, these are often buried deep in account settings, leaving most customers unaware of how their data is being used. This lack of transparency not only undermines consumer trust but also raises significant privacy concerns.

5. Low Interest on Savings Accounts

Saving money in a traditional bank account used to be a reliable way to earn interest and grow your wealth over time. Today, however, many banks offer interest rates so low that savers effectively lose purchasing power due to inflation. Meanwhile, banks use the funds deposited in these low-interest accounts to generate substantial profits through lending and investing.

For instance, a typical savings account might offer an annual percentage yield (APY) of 0.01% or 0.05%, while the bank earns several percentage points more by issuing loans or investing in higher-yield securities. The gap between what banks pay depositors and what they earn on those deposits is a core part of their profit model. Some customers turn to online banks or credit unions, which tend to offer higher rates, but the majority of savers still park their money in traditional accounts, often unaware that better options exist.

6. Predatory Mortgage Practices

The mortgage industry has seen some of the banking world’s most egregious abuses. From the subprime mortgage crisis of 2008 to ongoing issues with unfair loan terms, predatory mortgage practices remain a significant problem. Banks have been known to push customers into adjustable-rate mortgages (ARMs) that start with low rates but later balloon to unaffordable levels. This can lead to foreclosure, financial ruin, and long-term damage to credit scores.

Even after the housing crisis brought these issues to light, some banks have found ways to skirt regulations, offering loans with hidden clauses, high origination fees, and complicated terms that make it difficult for borrowers to understand the true cost of their mortgages. These tactics disproportionately affect first-time homebuyers, lower-income families, and those without the financial knowledge to navigate complex contracts.

7. Lack of Transparency in Investment Services

When consumers turn to banks for investment advice, they often assume their advisors are acting in their best interest. In reality, banks frequently have incentives to promote certain products over others—products that generate higher fees or commissions for the institution. These conflicts of interest mean that customers may end up in investments that are more expensive, less suitable, or underperforming compared to other available options.

Moreover, the fee structures for bank-provided investment services can be confusing. Account maintenance fees, trading fees, and expense ratios all eat into returns, but they’re not always clearly disclosed. Customers may not realize how much they’re losing to fees until they see the long-term impact on their portfolios.

8. Use of Bailout Money for Executive Bonuses

During times of economic crisis, governments often step in to bail out failing banks, using taxpayer money to stabilize the financial system. In theory, these bailouts should help preserve consumer deposits and maintain economic stability. In practice, however, some banks have used bailout funds to reward their executives with massive bonuses, even as ordinary consumers struggled through recessions.

This misuse of taxpayer money highlights a troubling lack of accountability in the banking sector. While millions of people faced job losses, foreclosures, and financial insecurity, bank executives who had overseen risky practices that contributed to the crisis were rewarded handsomely. This disparity fueled public outrage and led to calls for stricter oversight, though meaningful reform has been slow.

9. Aggressive Foreclosure Practices

When borrowers fall behind on mortgage payments, banks are often quick to initiate foreclosure proceedings, sometimes without exploring alternative solutions. While foreclosure is a necessary process in cases of default, some banks have been accused of rushing the process, failing to properly review documentation, or even engaging in robo-signing—an automated practice that led to errors and wrongful foreclosures.

In some cases, borrowers who were willing and able to modify their loans found themselves stonewalled by banks that preferred foreclosure as a faster, more lucrative solution. These aggressive practices not only destroy lives but also contribute to long-term economic instability, as foreclosed homes reduce property values and disrupt local communities.

10. Resistance to Regulation

Despite the widespread harm caused by some banking practices, the industry has consistently lobbied against stricter regulations. Banks often argue that increased oversight stifles innovation, reduces efficiency, and limits their ability to serve customers. In reality, many regulatory proposals are designed to protect consumers from predatory practices, improve transparency, and prevent the kind of systemic risks that lead to economic crises.

By resisting regulation, banks maintain the freedom to engage in many of the practices outlined above. Lobbying efforts are frequently well-funded and highly effective, ensuring that meaningful reform is slow to materialize. Meanwhile, customers continue to face hidden fees, predatory loans, and privacy risks.

Conclusion

Understanding these ten dirty secrets is the first step toward making more informed financial decisions. While it’s unrealistic to expect every consumer to become a banking expert, knowing what to watch out for can help you avoid common pitfalls, minimize fees, and protect your financial well-being. By demanding greater transparency, supporting regulatory reforms, and choosing financial institutions that prioritize customer interests, we can push the banking industry toward more ethical practices.

In the end, the more we know about the hidden mechanisms that underpin our financial system, the better equipped we’ll be to navigate it—and to hold banks accountable for the choices they make.

Are you intimidated by investing and don’t know where to start? Most people think you need deep pockets, ample free time, and a Wall Street education to start investing. I’m excited to tell you – none of that is true!

In fact, about 80% of American millionaires are self-made. They started with nothing, and learned to save and invest money from the ground up. Anyone can do it, and so can you.

The goal of investing is to simply buy assets that will increase in value over time. In this post we’ll be covering a basic five-step plan to start investing for beginners. It’ll include setting a budget, how and where to open accounts, and what assets to invest in. We’ll also cover a bunch of common investing questions towards the end.

Learning to invest might not be the most fun topic in the world, but I promise you it is worth it! Once you nail the basics and demystify some of the complexity, it turns out that building wealth is actually quite easy.

Why you need to start investing NOW!

Have you ever said to yourself, “I’ll start investing when I make more money.” Perhaps you’ve been concerned about market volatility as a result of recent current events (like during the COVID-19 global pandemic). It’s not that your hesitancy doesn’t make sense. The truth is that putting your investing journey on the back burner could cost you more than you realize.

In fact, experts estimate that ~40% of folks have experienced a financial loss due to procrastination. By waiting to invest, you could be missing out on potentially lucrative financial gains. Consequently, the timing of when you start investing could make a bigger impact on the amount you end up with than how much money you actually invest over time.

When it comes to investing for beginners, the earlier you start the better. The sooner you begin the longer your money will be working for you.

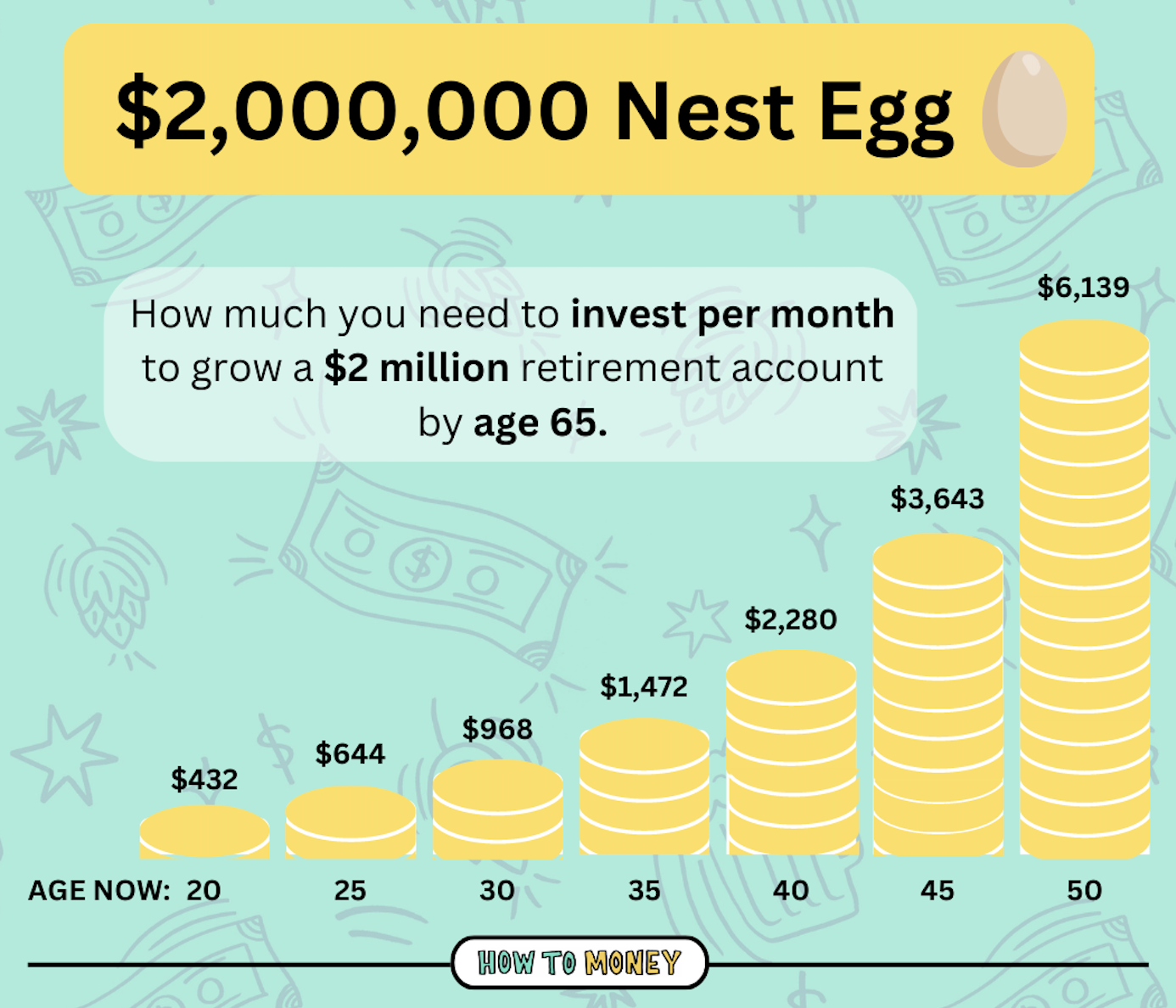

For example, check out the chart below. For a 20 year old to build a $2 million retirement portfolio, they would only need to save and invest about $432 per month. But for a 30 year old starting with nothing, that number is more than doubled!

For any older folks out there, this may seem disheartening. But while getting started early is a massive help, it’s also never too late to start investing for beginners!

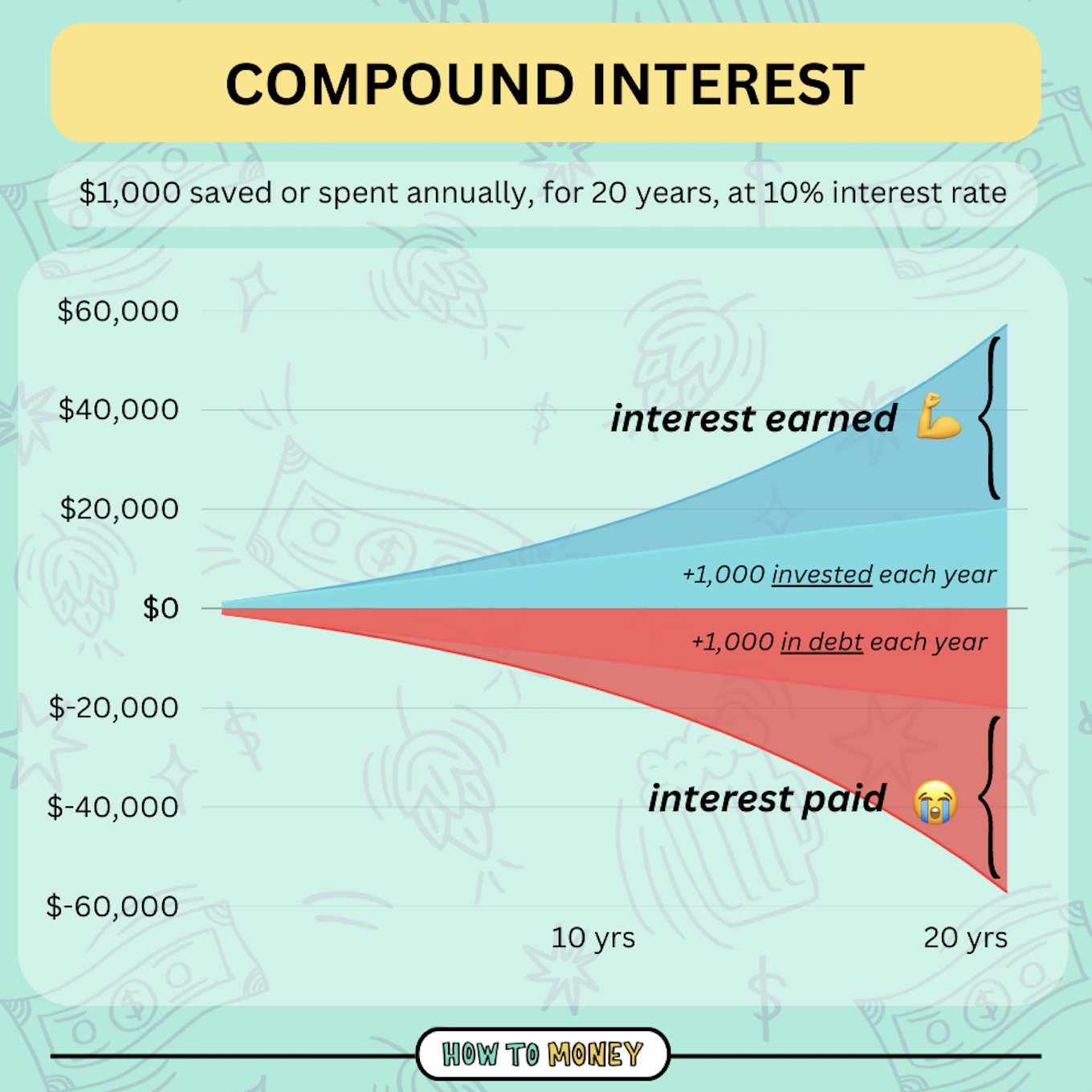

The Power of Compound Interest

The excitement of investing is that even a small account balance can grow into a large pile of cash over time. That’s because of the power of compounding interest. Compound interest is making money on top of the money you’ve already earned. You’re not just earning interest on your principal balance; your interest earns interest!

Here’s how it works: Let’s say you have $2,500 in a savings account that earns 5% in annual interest. In year one, you’d earn $125, giving you a new balance of $2,625. In year two, you would earn 5% on the larger balance of $2,625, which is $131.25—giving you a new balance of $2,756.25 at the end of year two.

This might seem like small numbers, but believe me – things really add up over time.

One other thing to consider is that compound interest can work for or against you. Here’s an illustration of how someone saving $1,000 per year earns amazing interest! But someone spending/borrowing each year PAYS big interest.

Bottom line: Make sure compound interest is working for you, not against you.

When it comes to compound interest, the more time you have the better. The sooner you start saving and investing for retirement (or any other goal for that matter), the more time you’ll have to take advantage of the power of compounding. In a way, it’s kind of like free money.

Investing for Beginners – 5 Step Guide

Fortunately, there are countless ways to begin investing for beginners – with most of them requiring a minimal time commitment. Choose a strategy to get started investing depending on the amount you’ll invest, the time frames for your individual financial goals, and the level of risk that makes sense for you.

Here are some simple steps to help you get started on your investing journey:

1. Define Your Goals & Set Your Budget

As you start the process of investing, you’ll want to think about your goals so that you can determine a budget. Investment goals might include buying a house, funding your retirement, or saving for you or your child’s education. Remember, it’s only natural for your goals to change over time as your stage of life changes.

Most financial experts recommend investing 15% to 25% of your post-tax income. But before determining how much you want to set aside, take a close look at your monthly income and figure out how much money you have left over after paying all your expenses. I like to call this your margin. If you can only start with 5% to 10%, that’s OK – it’s better than 0%!

Starting small is better than failing to start.

It’s also important to mention that you shouldn’t start investing until you’ve got some cash on hand in a regular ol’ savings account. Establishing an emergency fund is vital before you start investing in the stock market. This is simply a fund where you set cash aside to make it available for an easy withdrawal – if needed. Establishing an emergency fund will act as a safety net in case you’re in a situation of having to sell off investments during a time of need.

2. Determine Your Risk Tolerance

While investing can produce great returns over time, it also comes with risk. In this case, risk is merely the potential for your investments to lose value. If you invest $1,000, it might be worth $850 at the end of the year. That sounds awful, right? On a short timeline, investing comes with real risk. The longer your investing horizon, however, the less risky that decision becomes.

As an investor, it’s up to you to decide how much risk you’re willing to take on.

For instance, a conservative investor usually has a lower risk tolerance and wants to put their money into investments with guaranteed returns. On the other hand, an aggressive investor commonly has a higher risk tolerance and is willing to risk more money for the possibility of better returns. The bigger the risk, the bigger the reward, etc.

Considerations such as age, investment goals, and income are generally used by financial advisors to help investors determine their risk tolerance. Once you determine your risk tolerance, you’ll have a clearer picture of what types of investment purchases you’re most comfortable with.

It’s important to note that there is a risk to not investing too. We’ve all seen the impact that inflation can have on our purchasing power. When your pay goes up by 3% a year but your grocery bill soars by 12%, that’s a tough pill to swallow. The persistent reality of inflation is a real risk to your money and investing helps you mitigate that risk.

*Time* Can Lower Your Risk

Taking advantage of time is one of the ways you can decrease your risk while increasing your reward. History shows that the longer you keep your money invested, the greater your chances of enduring any downturns.

When your earnings compound, your investment gains expand tremendously over time. Long-term investments are frequently thought to be less speculative and risky than short-term investments, as they are less likely to fluctuate in value in the short-term.

Let’s break down the secret sauce that makes investments less risky — time. As history has shown, if you invested in the stock market for one year, your chance of losing money would be greater than 25%. However, if you invested for 10 years, that percentage drops dramatically to 4%, and after 20 years to 0%.

*Diversification* Can Lower Risk

Another way to lower risk is diversifying your investments. This is like spreading your eggs across multiple baskets.

One hundred years ago, investors heavily relied on stock brokers and fund managers to advise them on which stocks/bonds would make up a diversified portfolio. But thankfully these days, with modern technology advancements, diversifying your investments is quite easy!

We’ll dive into diversification via index funds a little later on. And you’ll be happy to know that some of the broadest and most diversified index funds available also have the highest average returns over long terms.

3. Open an Investing Account (or several)

Now we’re going to talk about what type of accounts you can open and a little about how each one works. Ideally you want to start off with any accounts that have tax advantages, as minimizing tax savings can help your investments grow faster.

401(k) Retirement Accounts:

One of the most convenient ways to begin investing is through an employer-sponsored 401(k) plan (or 403(b) if you work for a nonprofit or government entity). It’s especially beneficial if your job offers a match, which is essentially free money.

Check to see if your employer offers any type of retirement plan. If so, it should be seamless to set up a deduction from your paycheck. All you’ve got to do is figure out how much you want to contribute and make it happen.

Benefits of a 401(k) or 403(b) plan:

Paycheck deductions: Money is taken out of your paycheck *before* you get paid. This truly is a “set and forget” type of investing account. The more you automate your investments, the easier wealth building is.

Tax Advantages: Traditional 401(k) plans reduce your taxable income for the years you are investing. Paying less in taxes means your money grows at a faster rate (even though you will have to eventually pay taxes, later)

Employer matching: Some employers offer additional money if you contribute to your workplace retirement plan. If your work offers this, take advantage, ASAP!

You are in control of the money! When you leave your employer, you can “roll over” the money or bring the account with you to another employer.

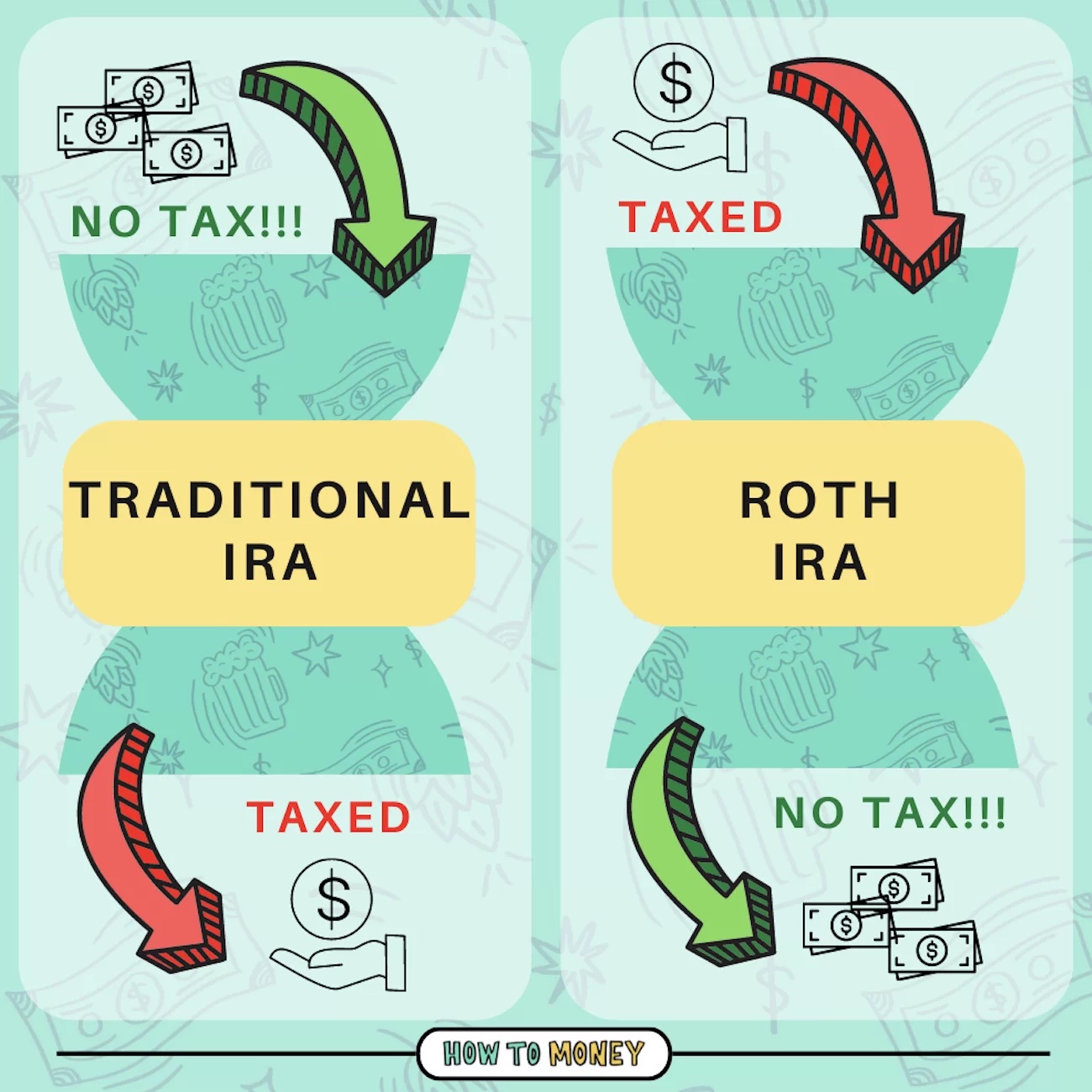

Traditional IRA and Roth IRA:

Another way to jumpstart your investing is through a personal retirement savings account, like an Individual Retirement Account (IRA) or Roth IRA. They’re offered by a variety of financial institutions and are simple to set up online.

Be aware that the IRS limits the amount you can add to each of these accounts on a per year basis. Also, these limits tend to be adjusted yearly so be sure to check the account limits on your preferred plan to adjust your budget accordingly.

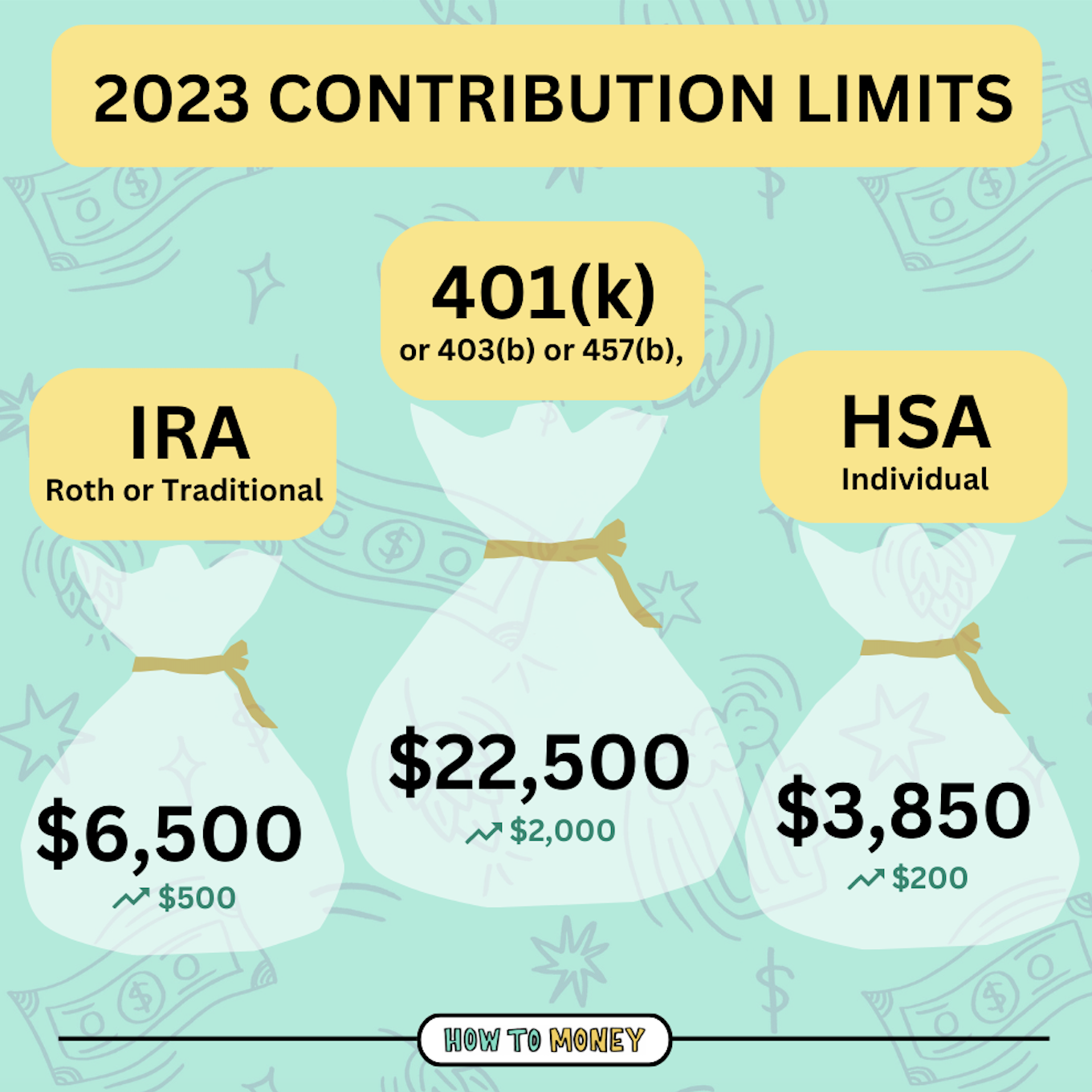

For 2023, the 401(k)-contribution limit is $22,500 (before employer match) and $6,500 for an IRA.

Older workers (those over age 50) can add an additional $7,500 to a 401(k) as a catch-up contribution, while an IRA allows an additional $1,000 contribution.

Income Limits – How much money you earn will determine your eligibility to contribute to a Roth or Traditional IRA. The IRS sets income limits that restrict high earners. The limits are based on your modified adjusted gross income (MAGI) and tax-filing status.

Roth IRA income limits for the 2023 tax year are $153,000 (was $144,000 in 2022) for single filers and $228,000 ($214,000 in 2022) for married couples filing jointly.

There are no income limits for Traditional IRAs – meaning you can contribute no matter how much money you earn. However, there are income limits for tax deductible contributions.

Brokerage Accounts

A brokerage account is another type of investment account that allows individuals to buy and sell things like stocks, bonds, mutual funds, and exchange-traded funds (ETFs). These accounts have no tax advantages, so we always recommend funding the above mentioned accounts first!

You can open a brokerage account online with little to no money up front in most cases. There is no limit on the number of brokerage accounts you can have or the amount of money you can put into your account annually.

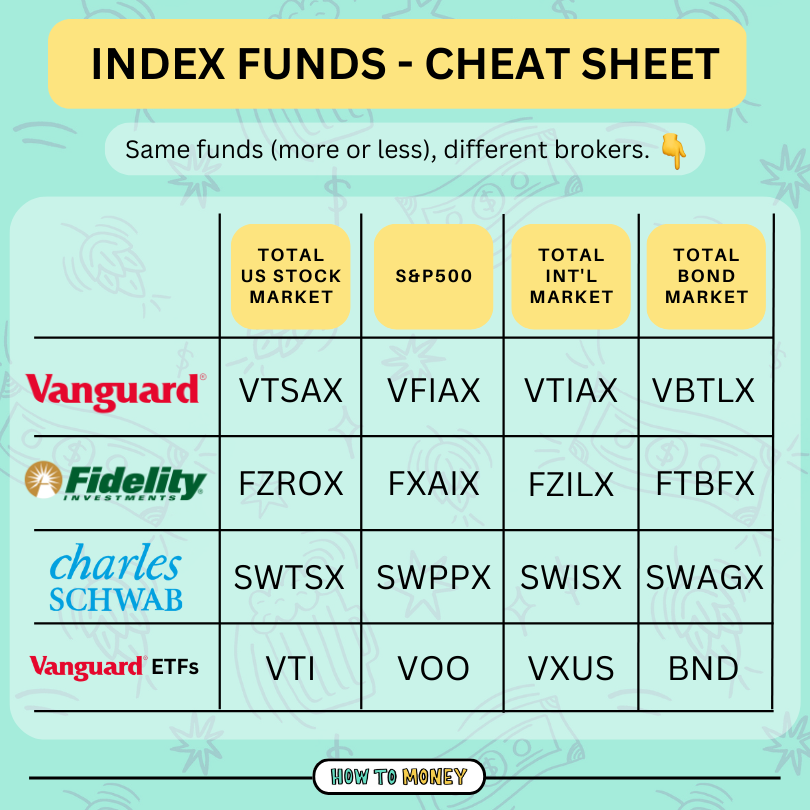

Also, there should be no fee associated with opening an account. We recommend Vanguard and Fidelity mostly, as these are the largest brokers with no account fees. Modern “robo-advisors” are good options also. M1 Finance and Betterment are two of the best in that category. We’ll get into more detail about these low cost brokers below!

After you’ve decided where you are going to invest, now it’s time to choose what to invest in. First, let’s quickly review what stocks and bonds are:

Stocks – A stock is a share of ownership in a single company that is publicly traded. Stocks can also be referred to as equities. Stocks can be purchased for a share price, which can widely range based on the value of the company.

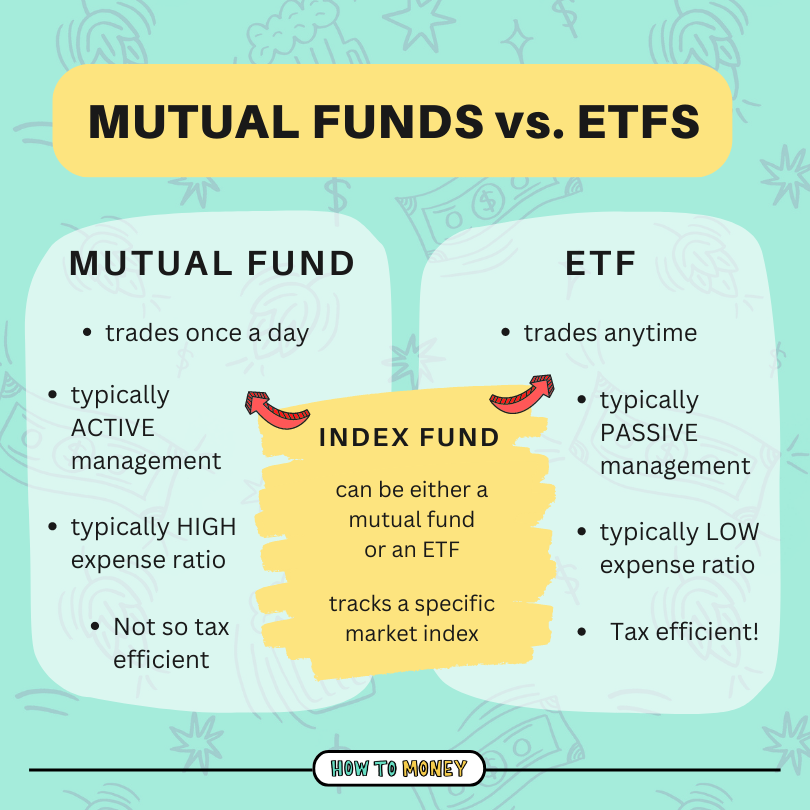

[RISK FACTOR] —> If your savings goal is 20+ years away (like retirement), it probably makes sense for a majority of your money to be in stocks. However, picking individual stocks can be complicated and time consuming. As a result, most people find that the best way to invest in stocks is to buy a giant basket of stocks via low-cost stock mutual funds, index funds, or ETFs [see below].

Bonds – When you purchase a bond, you are providing a loan to a company or government entity. That company/entity then agrees to pay you back in a certain number of years and during that time you earn interest.

[RISK FACTOR] —> Bonds are typically a lower-risk investment than stocks because you know the payback date and how much you’ll earn. But, over the long run bonds come with less upside compared to stocks. Depending on your age and your specific goals, bonds should make up either a larger or smaller percentage of your investment portfolio (less bonds for younger folks, more bonds for older folks).

Now let’s talk about mutual funds and ETFs. Think of these as pre-packaged portfolios that contain hundreds (sometimes thousands) of stocks and bonds inside of them…

Mutual Funds – A mutual fund is a mixture of investments packaged up and sold together. The idea is that you are mutually pooling your money with other investors to buy stocks, bonds, and other investments. Opting for a mutual fund allows you to bypass the work of picking individual stocks and bonds – instead, you’re buying a diverse collection in a single transaction.

[RISK FACTOR] —> Because you’re spreading money across a massive pool of stocks, mutual funds are generally less risky than individual stocks. They are diversified!

ETFs (exchange-traded funds) – Similar to a mutual fund, an ETF bundles many individual investments together. The difference is that ETFs trade throughout the day like a stock and are purchased for a share price. ETFs often track a certain sector, index, commodity, or other asset. An ETF’s share price is often lower than the minimum investment requirement of a mutual fund, which makes ETFs a good option for new investors or folks starting with small budgets.

[RISK FACTOR] —> The biggest risk in ETFs is market risk. Meaning the markets go up and the markets go down. ETFs diversify risk by tracking different companies in a sector or industry in a single fund.

Index Funds – As one of the easiest ways to invest (especially for beginners), index funds are ideal investments for long-term investors. They are a type of mutual or ETF fund that tracks the returns of a market index such as the S&P 500. When you take the index fund route, you are investing in all the companies that comprise a specific index, giving you a more diverse portfolio than if you bought individual stocks. Index funds have lower expenses and fees than actively managed funds and follow a passive investment strategy. The S&P 500 Index acts as a U.S. stock market benchmark. The index has posted a historic annualized average return of around 11.88% since its 1957 inception through the end of 2021.

[RISK FACTOR] —> The odds that an index fund loses everything are very low because they are often so diversified. Index funds are known for outperforming actively managed mutual funds, especially when the low fees are taken into consideration.

5. Keep Investing (Dollar-cost averaging or automate)

Once you start investing, the key is to remain consistent over a long period of time to ensure that you are successful. Setting up automatic transfers so that they happen every two weeks or at the end of each month is the best way to ensure your success as an investor. Even modest contributions, when made regularly, can pay off in a big way over the long term.

Another method that may work best for you is called dollar-cost averaging. This practice involves investing a set dollar amount on a regular basis. Don’t worry about what’s happening in the market – just keep buying! This helps to create a disciplined investing habit in your life. By investing regularly but also spreading out your stock or fund purchases across time, you can use dollar-cost averaging to lessen the impact of volatility in your life. It’s also clearly easier to invest a little every time you get paid!

As you continue to grow as an investor, it’s more important to review the progress you’re making toward your goals over time, as opposed to tracking short-term highs and lows. Basically, don’t check your balance every month. That snapshot doesn’t offer enough information. What the market did in a particular day should have no impact on your life!

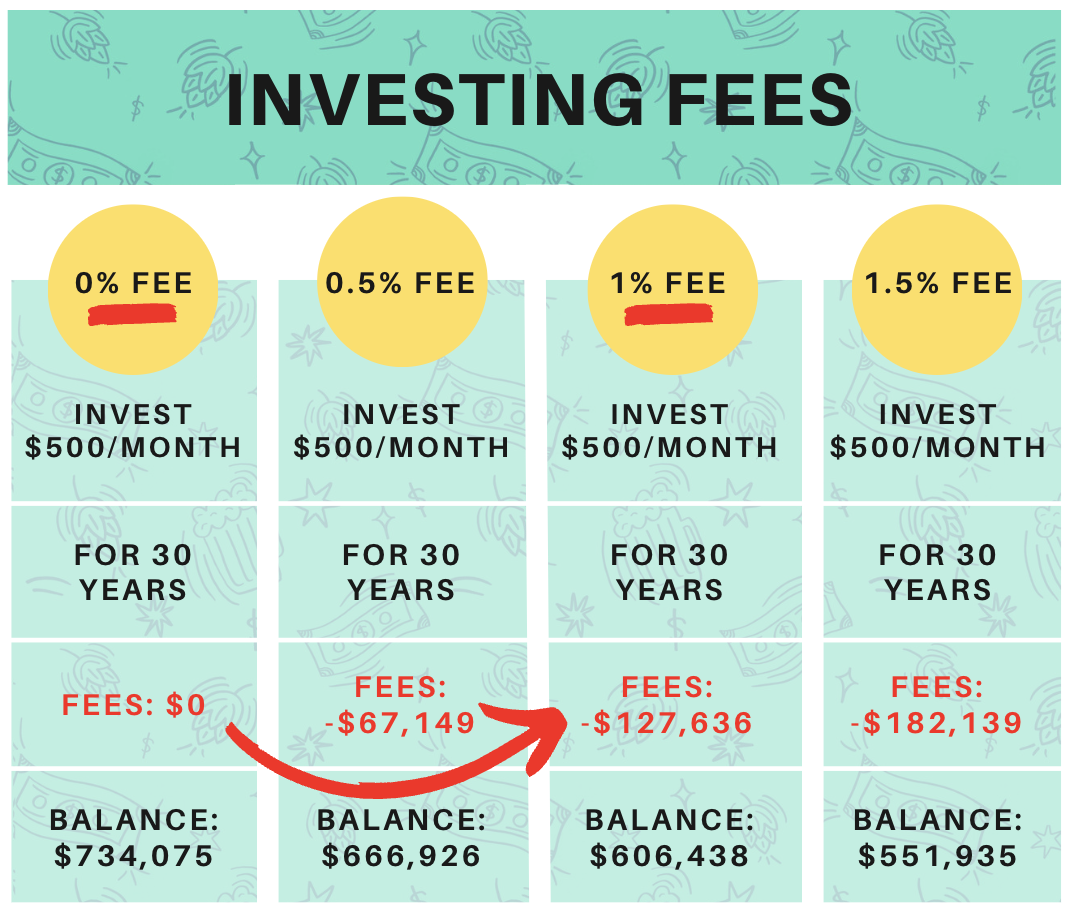

Avoiding Brokerage Fees

There’s no shortage of fees when it comes to investing! Common investment and brokerage fees include trade commissions, mutual fund transaction fees, expense ratios, sales loads, management or advisory fees, inactivity fees, research and data subscriptions, trading platform fees, paper statement fees, account closing or transfer fees, and 401(k) fees.

We HATE paying fees! They rob you of your investment returns.

Even a small brokerage fee can add up over the long haul. For example, you might think that a 1% commission doesn’t sound like much. However, if you invest for 30+ years that could eat away over $100,000 of your earnings!

You can avoid or minimize brokerage account fees by choosing an online broker that offers no account fees and commission-free trading. We’ve listed some in the FAQ below under Best Brokers for Beginners.

Another way to avoid fees is to passively manage your investments. Financial advisors can help solve complex problems within HUGE multimillion dollar portfolios. But for most folks (especially beginners just starting out) there is no need to involve an advisor. It’s not that they can’t be helpful. But it would be better to funnel the money you would have paid a professional into your investments instead!

Investing for Beginners FAQ:

Learning to invest can be overwhelming. But, YOU ARE NOT ALONE! Take your time and continue digesting bits of information here and there. After a while, you’ll start to pick up new terms and understand quickly.

Here are a bunch of beginner questions that might help…

Can you invest with just a little money?

Yes! Contrary to popular belief, you don’t need piles of cash to begin investing. You can start with as little as $1. For some folks, investing even $10 can feel like they’re stretching their budget too thin. But the amount of money you’re starting with isn’t as important as being financially prepared to invest money regularly over time.

Due to the power of compounding interest, investing is more about how much time you have, as it is about how much money you start with. So, once you’ve got that emergency fund in hand, even if you’ve only got a few bucks a month that you can contribute, go ahead and get started!

How much will you need for retirement?

The ability to truly “retire” will depend on many factors and everyone’s situation is unique. Of course, there is no shortage of benchmarks and guidelines for how much you need to retire on the internet. Some are more helpful than others.

One helpful rule of thumb is to work towards amassing 25x your annual expenses. For example, let’s say your annual spending is about $80,000 each year. This means you’ll want to save up about $2 million for retirement ($80K x 25). Studies have shown this is a safe estimate, also known as the 4% rule.

This may seem like an overwhelming number to save. But remember, compound interest is on your side. It’s the difference between saving and investing. Just begin making small and consistent contributions and you’ll be amazed how things grow over time.

What are the best brokerage accounts for beginners?

We recommend low-cost brokerage firms.

Fidelity is awesome. Free to open accounts, free to buy most funds, and they also host a handful of ETFs with no or very low management fees!

Charles Schwab has been around for decades. They are the 3rd-biggest broker (behind the ones we already mentioned).

If you’re looking for a really slick interface, M1 is a great investing app. And if you’d like a bit more hand-holding while still keeping fees low, robo-advisors can be a great solution.

Being a good investor isn’t about picking skyrocketing stocks and having the perfect timing. In fact, it’s rarely about making the right moves, and more about avoiding the wrong ones.

When asked for their biggest investing mistake, most seasoned investors responded, “I should’ve started earlier.” So by just reading this post and getting started, you’re already taking action and avoiding further delay!

As a long-term investor, you will live through several market crashes. But that’s OK, because you will also live through an equal amount of awesome market recoveries!

Market volatility is going to happen and can be created by unexpected economic news, changes in monetary policy, and political/geopolitical events. These are all things that are outside of your control. Just remember to stay calm and understand that this is most likely a temporary situation in the markets.

Here are a few things you can do to best prepare yourself during market volatility:

When the market crashes:

Review your financial goals

Build up your emergency fund

Don’t panic sell

Be opportunistic

Consider investing MORE (crashes are excellent buying opportunities)

If you are comfortable with money and have a basic understanding of investing, you’re probably fine managing your accounts on your own. The hardest part of investing is *waiting.* Picking accounts and buying index funds is quite simple, so there’s usually no need for an advisor (IMO!)

However, if you’re unsure of how to manage your finances or confused about how to make investments (even after reading this article), it could be worth hiring a financial advisor.

At different major milestones in your life, such as having kids, earning a promotion/large bonus, or inheriting money, you might want to consider chatting with an expert. It can be tough to know what to do when more money flows into your life!

Hiring advisors comes with a cost. And some of them might try to sell you costly products you don’t need. Our advice is to take your time selecting someone you trust. They should be a financial fiduciary (legally obligated to only recommend things in your best financial interest).

Still not sure whether you need to hire an advisor? Take a financial advisor quiz to help you determine your needs.

What is a Robo-Advisor?

Think of robo-advisors as apps that help manage your portfolio. They automate management so you can take a back seat when it comes to rebalancing, transferring money, or investing funds.

Robo-advisors can help create a diversified portfolio of low-cost mutual funds or ETFs that is suited to your needs after you provide some information about your goals, timeline, and risk tolerance. Most robo-advisors have fees, although some of them are free (that’s why we recommend M1 Finance – no fees!)

If you think investing in the stock market is hard, times that by 10 and that’s how difficult real estate investing is to master. 🤣 All jokes aside, we recommend learning the basics and starting small with tax advantaged investing accounts before jumping into real estate.

That being said, real estate can be amazing for growing wealth. Investors earn money from rental revenue, appreciation, and some real estate investments offer tax advantages. Passive income, consistent cash flow, tax advantages, diversification, and leverage are all advantages of real estate investing.

There’s a big learning curve with investing in real estate. BiggerPockets is a great place to start – it’s the biggest online network of real estate investors. They also have a podcast that covers all types of ways to make money in real estate.

And here’s a HUGE post about the process to buy a rental property. It takes a lot of time and effort, but it’s all worth it in the end!

Despite all the advantages of real estate investing, there are some disadvantages. One of the most significant is a shortage of liquidity (hard to sell a property at the drop of a hat). A real estate deal can take months (or years) to research and close, as opposed to a stock or bond transaction, which can be finished in seconds.

Trying to build wealth while paying off debt is like swimming against a strong current. No matter how much effort you put into getting ahead, debt will continue to compound against you and pull you backwards.

This is why we created the 7 money gears. Think of it as an order of operations to follow. If you have high-interest debt, (credit cards, or anything above ~7% interest) you’ll want to prioritize paying that off before investing. **Except for 401(k) accounts or retirement plans that you get matching dollars from your employer.**

Not all debt is bad (check out good debt vs. bad debt examples here) so it really depends on your individual situation and numbers for when investing makes sense.

The Bottom Line

Beginning to invest can be the single wisest financial move you ever make, laying the groundwork for a lifetime of financial security and a peaceful retirement. Remember, you can’t “save” your way to retirement. You need to learn how to get your money to make more money – that’s where the power of compounding comes into play!

It’s never too late to start investing, no matter how old you are or where you are in life. You can’t undo what you’ve done or haven’t done, but you can change your future for the better. So, what’s holding YOU back? There’s no better time than now to start investing. Your future self will be grateful.

What Next? 3-Step Action Plan Moving Forward:

Determine how much you can save/invest monthly —> Create a budget. Review your finances and your spending plan. How much can you invest on a monthly basis?

Create a regular schedule —> Set up a regular transfers to your investment account and stick with it. Base the timing around when you get paid and when your bills are due.

Increase your contributions over time —> It’s great that you can start investing with only $10 a week, but that’s not going to be enough long term. If you expect to reach your goals, you need to increase your investments over time. Work to creatively find ways to save more money to invest.

In today’s rapidly evolving financial landscape, mastering personal finance isn’t just about saving money—it’s about making strategic decisions that align with modern economic realities. This comprehensive guide will walk you through everything you need to know about managing your finances in 2024.

🎯 The New Rules of Money Management

The financial world has transformed dramatically. Digital banking, cryptocurrency, and automated investing have changed how we interact with money. But the fundamentals of smart money management remain crucial. Here’s your roadmap to financial success in 2024.

The 50/30/20 Rule: Reimagined for 2024

Traditional budgeting rules need modern updates. Here’s how to adapt the classic 50/30/20 rule for today’s economy:

50% Essential Expenses

Housing (including utilities and internet)

Transportation (including remote work setup)

Groceries and essential supplies

Healthcare and insurance

30% Lifestyle Choices

Digital subscriptions

Entertainment

Shopping

Personal care

Side hustle investments

20% Financial Goals

Emergency fund

Retirement savings

Debt repayment

Investment portfolio

Future planning

💡 Smart Money Moves for 2024

1. Build a Digital-First Financial Foundation

The digital economy demands a modern approach to banking:

Set up a high-yield online savings account

Use budgeting apps for real-time expense tracking

Automate bill payments and savings transfers

Consider digital payment solutions for better rewards

Monitor your credit score through free online services

2. Emergency Fund 2.0

The traditional three-month emergency fund might not cut it anymore. Consider:

Building a 6-month basic expenses fund

Creating a separate “opportunity fund” for career transitions

Keeping some savings in inflation-protected investments

Maintaining a portion in easily accessible cash

Setting up multiple savings buckets for different purposes

3. Debt Management Strategies

Smart debt management is crucial in a high-interest environment:

Prioritize high-interest debt repayment

Consider debt consolidation if rates are favorable

Protect your financial future with modern security measures:

Use strong, unique passwords for all financial accounts

Enable two-factor authentication

Regular monitoring of all accounts

Secure Wi-Fi networks for financial transactions

Updated anti-virus and security software

Insurance Evolution

Modern insurance needs have evolved:

Health insurance with telehealth coverage

Life insurance with living benefits

Disability insurance for gig workers

Cyber insurance for digital assets

Identity theft protection

📱 Leveraging Technology for Financial Success

Essential Financial Apps for 2024

Create your financial tech stack:

Budgeting and Tracking

Expense tracking apps

Investment monitoring tools

Bill payment organizers

Saving and Investing

Automated investing platforms

Roundup savings apps

Cashback reward programs

Financial Education

Learning platforms

Market news apps

Financial planning tools

🎓 Continuous Financial Education

Stay Informed and Adaptable

The financial world evolves rapidly. Stay current through:

Financial podcasts

Online courses

Professional webinars

Industry newsletters

Expert blogs and forums

🎯 Setting and Achieving Financial Goals

SMART Goals for 2024

Make your financial goals:

Specific: Clear, defined objectives

Measurable: Trackable progress

Achievable: Realistic targets

Relevant: Aligned with your life goals

Time-bound: Set deadlines

🌟 Future-Proofing Your Finances

Planning for Tomorrow

Consider long-term strategies:

Retirement planning adjustments

Career development investments

Skills upgrading for future opportunities

Passive income stream development

Estate planning updates

🔄 Regular Financial Check-ups

Monthly Financial Health Checklist

Review budget adherence

Check investment performance

Monitor credit score changes

Update financial goals

Adjust strategies as needed

🎉 Conclusion: Your Financial Success in 2024

Managing personal finances in 2024 requires a blend of traditional wisdom and modern strategies. By staying informed, leveraging technology, and maintaining disciplined habits, you can build a strong financial foundation for your future.

Remember: Financial success isn’t about following every trend—it’s about creating a sustainable system that works for your unique situation. Start implementing these strategies today, and watch your financial health transform throughout the year.

If you’re looking to grow your wealth and secure your financial future, investing is one of the most powerful tools at your disposal. However, the world of investing can seem overwhelming at first. This guide will help you understand the fundamentals of smart investing and how to get started on your investment journey.

Understanding the Basics of Investment

Before diving into specific investment strategies, it’s crucial to understand what investing really means. At its core, investing is the act of committing money or capital to an endeavor with the expectation of obtaining additional income or profit. Unlike saving money in a bank account, investing puts your money to work for you through various financial instruments.

Key Investment Vehicles

Stocks

Stocks represent ownership in a company and can provide returns through both price appreciation and dividends. While they can be volatile in the short term, historically, stocks have provided some of the highest long-term returns among all asset classes.

Bonds

Bonds are essentially loans you make to governments or corporations. They typically offer lower returns than stocks but provide steady income and are generally considered less risky. Bonds play a crucial role in portfolio diversification and risk management.

Index Funds

Index funds track specific market indices, offering broad market exposure with low fees. They’re an excellent choice for beginners and long-term investors alike, providing instant diversification and professional management at a fraction of the cost of actively managed funds.

Creating Your Investment Strategy

1. Define Your Goals

Are you saving for retirement, a house down payment, or your children’s education? Your investment goals will help determine your strategy, including how much risk you can afford to take and your investment timeline.

2. Assess Your Risk Tolerance

Understanding how much market volatility you can handle emotionally and financially is crucial. Your risk tolerance should influence your asset allocation—the mix of stocks, bonds, and other investments in your portfolio.

3. Diversify Your Portfolio

Don’t put all your eggs in one basket. Diversification across different:

Asset classes (stocks, bonds, real estate)

Sectors (technology, healthcare, finance)

Geographic regions (domestic and international markets) can help reduce risk while maintaining potential returns.

Smart Investment Practices

Start Early

The power of compound interest means that time is your greatest ally in investing. Starting early, even with small amounts, can lead to significant wealth accumulation over the long term.

Regular Investment

Consider dollar-cost averaging—investing fixed amounts at regular intervals—rather than trying to time the market. This strategy helps reduce the impact of market volatility on your investments.

Keep Costs Low

Investment fees can significantly impact your returns over time. Focus on low-cost index funds and ETFs, and be mindful of transaction fees and management expenses.

Managing Your Investment Portfolio

Regular Review

Review your portfolio periodically (quarterly or annually) to ensure it remains aligned with your goals and risk tolerance. This doesn’t mean making frequent changes—rather, it’s about staying informed and making adjustments when necessary.

Rebalancing

Over time, some investments may grow faster than others, throwing off your target asset allocation. Periodic rebalancing helps maintain your desired level of risk and potential return.

Common Investment Mistakes to Avoid

Emotional Decision Making: Don’t let fear or greed drive your investment decisions. Stick to your strategy, especially during market volatility.

Trying to Time the Market: Consistently predicting market movements is nearly impossible. Focus on time in the market rather than timing the market.

Neglecting Research: While you don’t need to be an expert, understanding basic investment principles and your specific investments is crucial for long-term success.

Getting Started

Build an emergency fund before investing

Take advantage of any employer retirement matching programs

Consider consulting with a financial advisor for personalized guidance

Start with broad-market index funds while learning more about investing

Keep educating yourself about financial markets and investment strategies

Conclusion

Successful investing isn’t about getting rich quickly—it’s about making informed decisions, staying disciplined, and thinking long-term. By understanding these fundamental principles and following a well-thought-out strategy, you can work toward building lasting wealth and achieving your financial goals.

Remember: The best investment strategy is one you can stick with through market ups and downs. Focus on your long-term goals, keep your costs low, and stay diversified. With patience and discipline, you can build a robust investment portfolio that serves your financial needs for years to come.

In today’s dynamic financial landscape, developing a sound investment strategy is crucial for building long-term wealth. This comprehensive guide explores proven investment strategies that can help you make informed decisions and achieve your financial goals in 2024 and beyond.

Understanding Your Investment Foundation

Before diving into specific strategies, it’s essential to establish your investment foundation based on your personal circumstances and goals.

Risk Assessment and Tolerance

Your investment strategy should align with your personal risk tolerance. Consider:

Your age and time horizon for investing

Financial goals and objectives

Current income and expenses

Emergency fund status

Overall financial stability

Core Investment Strategies

Diversification

Spread investments across different asset classes

Invest in various geographic regions

Consider multiple industries and sectors

Mix different market capitalizations

Include alternative investments when appropriate

Dollar-Cost Averaging

Invest fixed amounts regularly

Reduce impact of market volatility

Maintain a disciplined approach

Avoid emotional decision-making

Lower average cost per share over time

Value Investing in 2024

Focus on company fundamentals

Analyze price-to-earnings ratios

Evaluate debt levels and cash flow

Assess competitive advantages

Consider ESG factors

Modern Investment Opportunities

ESG (Environmental, Social, and Governance) Investing

Focus on sustainable businesses

Consider social responsibility

Evaluate corporate governance

Tap into growing market opportunities

Build long-term value

Technology Sector

Artificial Intelligence companies

Cloud computing services

Cybersecurity firms

Blockchain technology

Internet of Things (IoT) innovations

Real Estate Investment Strategies

REITs (Real Estate Investment Trusts)

Commercial property investments

Residential real estate

Real estate crowdfunding

Property technology companies

Risk Management Techniques

Portfolio Rebalancing

Regular portfolio review

Maintain target asset allocation

Adjust for market changes

Consider tax implications

Stay aligned with goals

Hedging Strategies

Use of stop-loss orders

Options strategies

Inverse ETFs

Precious metals allocation

Cash position management

Emerging Trends to Consider

Digital Assets

Cryptocurrency investments

NFTs (Non-Fungible Tokens)

Digital payment systems

Fintech innovations

Digital banking platforms

Sustainable Investments

Renewable energy

Clean technology

Sustainable agriculture

Water conservation

Green infrastructure

Investment Tips for Success

Research and Due Diligence

Study market trends

Analyze company reports

Monitor economic indicators

Follow industry news

Consult financial professionals

Long-term Perspective

Avoid short-term thinking

Focus on fundamental value

Stay committed to strategy

Ignore market noise

Regular strategy review

Conclusion

Successful investing in 2024 requires a balanced approach combining traditional wisdom with modern opportunities. Focus on building a diverse portfolio that matches your risk tolerance and financial goals. Remember that successful investing is a marathon, not a sprint. Regular review and adjustment of your strategy, while maintaining a long-term perspective, will help you navigate market changes and achieve your financial objectives.

Start implementing these strategies gradually, and consider consulting with financial professionals for personalized advice. Keep learning about new investment opportunities while staying grounded in fundamental investment principles.

Would you like me to expand on any particular section or add more specific details about certain investment strategies?

In today’s digital age, earning money online has become more accessible than ever. Whether you’re looking to supplement your current income or build a full-time online business, there are numerous opportunities available. This guide explores ten legitimate and proven methods to generate income online.

1. Freelancing: Your Skills, Your Terms

Freelancing has emerged as one of the most reliable ways to earn online. Platforms like Upwork, Fiverr, and Freelancer.com connect skilled professionals with clients worldwide. Popular freelancing niches include:

Content writing and copywriting

Graphic design and illustration

Web development and programming

Digital marketing and SEO

Virtual assistance

Success in freelancing comes from building a strong portfolio, maintaining high client satisfaction rates, and consistently delivering quality work on time.

2. Digital Product Creation and Sales

Creating and selling digital products offers excellent passive income potential. Once created, these products can generate revenue indefinitely with minimal ongoing effort. Popular digital products include:

Online courses and tutorials

Ebooks and digital guides

Templates and printables

Stock photos and videos

Music and sound effects

Platforms like Gumroad, Teachable, and Etsy make it easy to sell digital products to a global audience.

3. Affiliate Marketing: Earn Through Recommendations

Affiliate marketing involves promoting other companies’ products or services and earning a commission for each sale made through your referral. Key steps to success include:

Choosing the right niche and products

Building a trusted platform (blog, YouTube channel, or social media presence)

Creating valuable content that solves problems

Implementing effective SEO strategies

Being transparent about affiliate relationships

Amazon Associates, ClickBank, and Commission Junction are popular affiliate networks to start with.

4. YouTube Content Creation

YouTube has become a significant platform for earning online income. Successful YouTubers generate revenue through:

Ad revenue through the YouTube Partner Program

Sponsored content and brand deals

Merchandise sales

Channel memberships

Super Chat and Super Stickers during live streams

Focus on creating high-quality, engaging content consistently and building a loyal audience.

5. Online Course Creation and Teaching

The e-learning industry continues to grow rapidly. Creating and selling online courses allows you to share your expertise while generating income. Consider:

Identifying your area of expertise

Researching market demand

Creating comprehensive, high-quality content

Marketing your course effectively

Gathering and implementing student feedback

Platforms like Udemy, Skillshare, and Coursera provide ready-made audiences for course creators.

6. Print-on-Demand Business

Print-on-demand services allow you to sell custom-designed products without holding inventory. Popular items include:

T-shirts and apparel

Mugs and phone cases

Wall art and home decor

Custom notebooks and stationery

Accessories

Services like Printful, Redbubble, and Merch by Amazon handle production and shipping, letting you focus on design and marketing.

7. Social Media Management

As businesses increasingly prioritize social media presence, demand for skilled social media managers continues to grow. Services typically include:

Content creation and scheduling

Community engagement

Analytics and reporting

Strategy development

Paid advertising management

Start by managing accounts for small businesses and build your portfolio gradually.

8. Website Flipping

Website flipping involves buying existing websites, improving them, and selling them for a profit. Success requires:

Understanding website valuation

Identifying undervalued properties

Implementing effective improvements

Marketing to potential buyers

Negotiating profitable deals

Platforms like Flippa and Empire Flippers facilitate website buying and selling.

9. Virtual Event Planning and Hosting

The rise of remote work has created opportunities in virtual event planning. Services might include:

Corporate webinars and conferences

Online workshops and seminars

Virtual team-building events

Digital product launches

Online networking events

Focus on delivering seamless experiences and solving common virtual event challenges.

10. Subscription-Based Services

Recurring revenue models provide stability and predictability. Consider offering: